The Two Systems of Thought

Kahneman introduces us to the metaphor of two agents inside our heads:The interplay between these two systems defines much of human judgment and decision-making. While System 1 is efficient, it is also the source of many systematic errors in reasoning.

Heuristics and Biases

One of the book's most significant contributions is the detailed exploration of heuristics and biases. Because System 1 seeks quick answers, it often substitutes difficult questions with easier ones, leading to predictable errors:These cognitive shortcuts served our ancestors well in survival situations but often lead to irrational choices in the modern world of finance, medicine, and law.

Prospect Theory and Loss Aversion

Kahneman, along with his late collaborator Amos Tversky, developed Prospect Theory, which challenges the traditional economic assumption that humans are rational actors ("Econs"). Instead, he argues we are "Humans" who value gains and losses differently:This asymmetry explains why people hold onto losing stocks too long or buy insurance against unlikely disasters.

The Two Selves: Experiencing vs. Remembering

Towards the end of the book, Kahneman distinguishes between two selves that govern our happiness:Crucially, the Remembering Self often dominates our future choices, leading us to pursue vacations or careers that look good in memory rather than those that provide the most sustained enjoyment.

Conclusion: The Value of Slowing Down

The ultimate takeaway from Kahneman's work is not that we should distrust our intuition entirely, but rather that we must recognize when to engage System 2. In high-stakes situations involving statistics, long-term planning, or significant financial risk, relying on gut feeling is dangerous. By understanding the machinery of our minds—the lazy System 2 and the overconfident System 1—we can learn to spot the signs of cognitive bias, slow down our reasoning, and make better, more rational decisions. While we cannot eliminate errors, awareness is the first step toward mitigation.

接连出海,授权交易亮眼

回顾去年 6 月,迈威生物在国际化布局上扔出了第一张王牌,与 CALICO 就自主研发的 IL-11 单抗 9MW3811 签下了独家许可协议。这笔交易含金量十足,前者不仅能拿到 2500 万美元的一次性不可退还首付款,后续里程碑付款最高更可达 5.71 亿美元。

这还不算完,时隔仅仅三个月,公司又在心血管领域发力,就双靶点 siRNA 创新药 2MW7141 与 Kalexo 签订协议,合作金额最高可达 10 亿美元。接连两笔大额授权交易,足以证明迈威生物在研发管线上的硬实力获得了国际认可。

首付款虽香,难解近渴

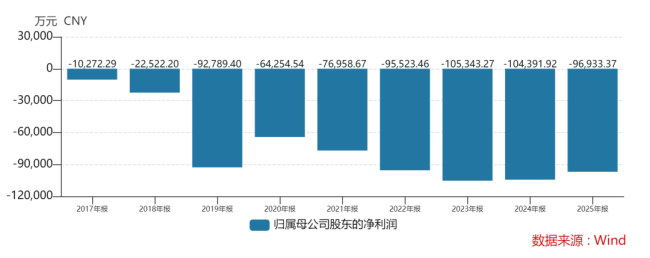

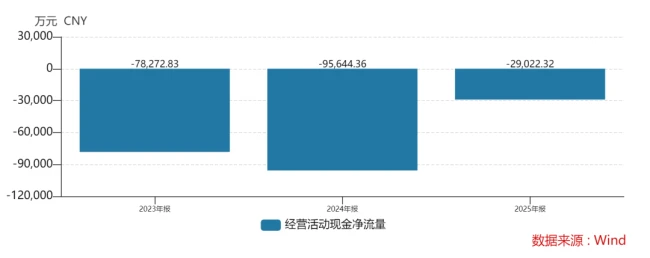

不过,账面上的数字再好看,也得落到口袋里才算数。对于Biotech 企业来说,光有首付款,远水还是解不了近渴,迈威生物管理层显然也清楚这一点。研发是个烧钱的无底洞,仅靠License-out 的首付款难以支撑长期的运营和扩张需求。

趁着业绩高涨的窗口期,公司选择了第三次递交港股 IPO 申请,试图通过资本市场输血。这步棋走得很明确,就是要利用当下的热度,尽快打通融资渠道,为后续发展备好粮草。

港股排队拥堵,前路未卜

但现实情况是,目前港股市场的入场券越来越难拿了。去年超 70 家生物医药企业递表港交所,场面可谓拥挤不堪。剔除已通过聆讯的企业,仍有约 65 家在排队审核中,等待周期被大幅拉长。

在这种背景下,迈威生物不知道要等到何时才能成功敲钟。面对漫长的审核队列和充满不确定性的市场环境,如何平衡现金流与研发进度,将是考验公司生存智慧的关键。未来的路怎么走,还得看港交所的审批节奏以及公司自身的造血能力能否撑过这段等待期。